About six months out? This quick checklist covers credit tune-ups, budgeting with realistic payments, building cash for down payment and closing costs, and getting lender-ready—so you can move fast when the right home appears.

Option 1: Quick Win Post

Buying a home in ~6 months? Here’s your quick plan:

• Month 1: Pull all 3 credit reports, dispute errors, set a realistic budget.

• Month 2: Automate savings to a dedicated account; trim non-essentials.

• Month 3: Research neighborhoods, track prices, tour a few open houses.

• Month 4: Get pre-approved; gather tax returns, pay stubs, bank/asset statements.

• Month 5: Avoid big purchases or new credit; reinforce your emergency fund.

• Month 6: Choose your agent, line up an inspector/attorney (if needed), and prep to write offers.

Six months out is the sweet spot to de-risk homebuying:

• Financial readiness: Review all three credit reports, calculate DTI, and budget for down payment, closing costs, and moving.

• Savings engine: Automate transfers, trim recurring spend, consider a side gig for extra cushion.

• Market research: Compare neighborhoods by commute, schools, amenities; monitor list-to-sale dynamics and price trends.

• Lender power: Shop lenders, organize docs (W-2s, pay stubs, bank/asset statements), and secure a pre-approval.

• Risk control: Pause big purchases, avoid opening new credit, keep employment steady, and build a 3–6 month buffer.

• Team up: Hire a local agent; consider a real estate attorney (state-dependent) and line up a thorough inspector.

Preparation now = smoother offers, cleaner underwriting, and fewer surprises at closing.

Question: If you’re ~6 months from buying, what’s your top priority today?

A) Clean up credit & set a budget

B) Automate savings for down & closing

C) Research neighborhoods & price trends

D) Get a real pre-approval and organize docs

Answer: Pick the lever that shortens your path. Clear credit issues, build cash automatically, study the market, and lock a legit pre-approval so you can act fast when the right home hits.

You Decided to Buy a New Home – Here’s What You Need to do Next

Ready to start house hunting? Before open houses, build a strong foundation: tighten credit and savings, get pre-approved, define must-haves vs. deal-breakers, organize documents, and avoid common pitfalls like opening new credit or changing jobs. This guide walks you through each step so you can shop confidently and close smoothly.

Option 1: Quick Win Post

You’ve decided to buy a home—now what?

• Step 1: Credit & cash — review all three reports, fix errors, aim higher on score, pause big purchases.

• Step 2: Pre-approval — gather pay stubs, W-2s, bank statements, and shop lenders.

• Step 3: Define needs — must-haves, nice-to-haves, deal-breakers; research neighborhoods.

• Step 4: Get organized — keep docs in one digital folder; add proof of any extra income.

• Step 5: Avoid pitfalls — don’t change jobs or open new credit; stick to your budget.

• Step 6: Choose the right agent — and plan for surprises (appraisal, inspection, timelines).

Buying a home starts long before the first open house. Here’s the foundation that makes the rest easy:

• Financial health: Check your credit report for errors, target the best pricing, and hold off on big purchases that can inflate your DTI.

• Pre-approval as your “ticket”: Provide pay stubs, W-2s, tax returns, bank/asset statements, and debt details. A strong letter focuses your search and strengthens offers.

• Define the target: Clarify must-haves vs. nice-to-haves and deal-breakers. Research commute, schools, amenities, and future development.

• Paperwork ready: Centralize documents (and proof of extra income) to reduce underwriting friction.

• Avoid common mistakes: Don’t switch jobs, don’t open new credit lines, and don’t stretch beyond your comfort payment.

• Think ahead: Layout for remote work or a growing family, location for potential appreciation, and features that help resale.

Question: After deciding to buy, what’s your first move?

A) Clean up credit & build reserves

B) Get a full pre-approval

C) Define must-haves & target neighborhoods

D) Gather pay stubs, W-2s, and bank statements

Answer: Pick the step that removes your biggest bottleneck. Clean credit + real pre-approval + organized docs = stronger offers when the right home appears.

Planning to Buy a Home in the Next 12 Months? Focus on Your Credit Now

Ready to buy in a year? This month-by-month game plan covers credit, saving for down payment and closing costs, getting pre-approved, and touring smart—so you’re confident when it’s time to make an offer.

Option 1: Quick Win Post

Buying in the next 12 months? Start now.

• Month 1: Pull your credit and dispute errors. Aim 700+.

• Months 2–3: Automate savings for down payment + closing costs.

• Months 4–5: Pay down high-interest debt. No new accounts.

• Months 6–7: Set a realistic budget (taxes, insurance, HOA).

• Months 8–9: Get pre-approved and gather docs.

• Months 10–11: Tour with a great agent and take notes.

• Month 12: Make an offer, inspect, close.

A 12-month runway to homeownership beats rushing at the finish line. Here’s the framework I recommend clients follow:

• Credit first (Month 1): Pull all three reports, fix errors, target 700+ for better pricing.

• Liquidity (Months 2–3): Automate savings for down payment and 2–5% closing costs. Trim subscriptions and redirect windfalls.

• De-risk (Months 4–5): Pay down high-interest debt to improve DTI; avoid opening new credit.

• Reality check (Months 6–7): Model payment scenarios including taxes, insurance, HOA, and maintenance. Pressure-test at ±0.25% rate.

• Lender readiness (Months 8–9): Shop lenders, secure pre-approval, and keep docs in a shared folder.

• Execution (Months 10–11): Tour strategically, focus on days-on-market and price history, document pros/cons.

• Close strong (Month 12): Write a competitive offer inside your budget, order inspection, negotiate credits, and close.

Question: If you want to buy a home in 12 months, what’s your biggest focus today?

A) Getting my credit to 700+

B) Building a bigger down payment

C) Locking in a realistic monthly budget

D) Getting pre-approved and gathering docs

Answer: Pick the lever that moves your timeline most. Clean up credit errors, automate savings, price your monthly payment with taxes/insurance, and get pre-approved so you can act quickly when the right home appears.

Labor Day 2025 Housing Update: Mortgage Rates, Inventory & Is It Time to Buy?

Rates remain volatile, inventory is shifting, and buyer options are changing in many markets. Get the quick take on what this Labor Day snapshot could mean for your next move.

Option 1: Quick Win Post

Mortgage rates are back in the mid-6 percent range, and listings are up. Over Labor Day, buyers have leverage: more homes, fewer bidding wars, and motivated sellers.

If the payment fits your budget, now could be the time to make a move.

Rates have drifted into the mid-6 percent range, while active listings are higher than a year ago. That combo gives buyers leverage: more choice, fewer bidding wars, and negotiating power.

How to play it:

- First-time buyers: Lock if the payment fits, and ask for a float-down option before closing. Bring a fully underwritten pre-approval.

- Move-up buyers: Weigh the cost of staying (low rate, limited space) vs. moving (new payment, taxes, insurance). Target longer-days-on-market listings and ask for seller credits to buy down the rate.

- Equity-rich or cash-heavy: Push on price and concessions now; if rates dip later, refinance to optimize.

Bottom line: If the right home fits your budget, acting this Labor Day starts your equity clock sooner. You can refinance later if rates improve.

Question: If you were house-hunting this Labor Day, what matters most to you?

A) Lower mortgage rates

B) More homes to choose from

C) Negotiating power with sellers

D) Waiting to see what the Fed does next

Answer: Focus on the path that best matches your budget and timeline. If payment comfort is key, test your numbers at plus/minus 0.25 percent and ask for seller credits to buy down the rate. If selection matters, use today’s higher inventory to negotiate. Keep pre-approval current and be ready to move when quotes dip.

Home equity can be a powerful tool—but only when used smartly. Whether you’re refinancing, making home upgrades, or managing debt, discover strategies to unlock its potential in today’s market.

Option 1: Quick Win Post

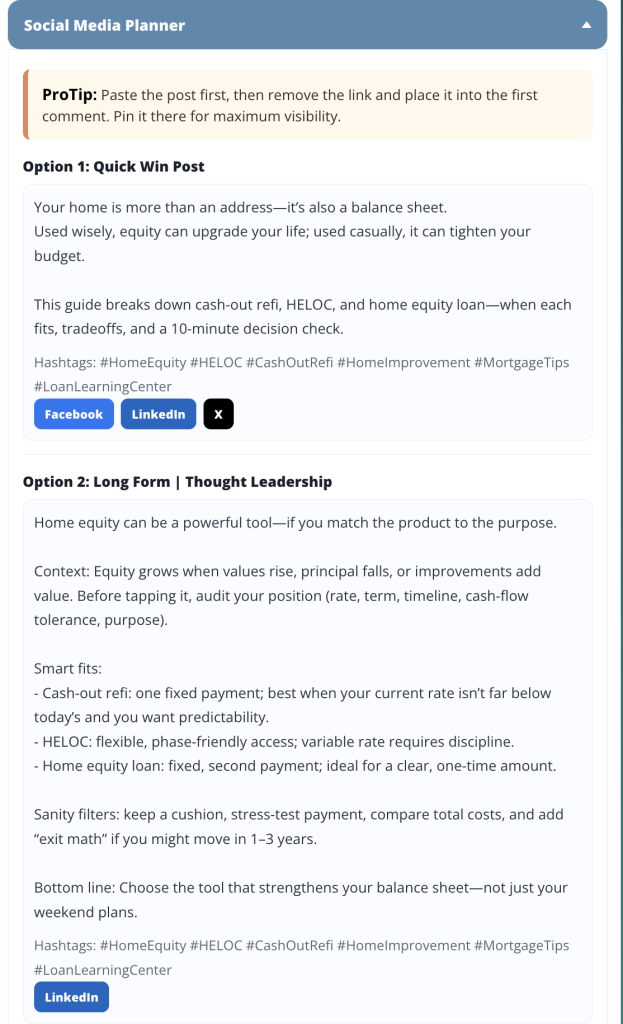

Your home is more than an address—it’s also a balance sheet.

Used wisely, equity can upgrade your life; used casually, it can tighten your budget.

This guide breaks down cash-out refi, HELOC, and home equity loan—when each fits, tradeoffs, and a 10-minute decision check.

Home equity can be a powerful tool—if you match the product to the purpose.

Context: Equity grows when values rise, principal falls, or improvements add value. Before tapping it, audit your position (rate, term, timeline, cash-flow tolerance, purpose).

Smart fits:

- Cash-out refi: one fixed payment; best when your current rate isn’t far below today’s and you want predictability.

- HELOC: flexible, phase-friendly access; variable rate requires discipline.

- Home equity loan: fixed, second payment; ideal for a clear, one-time amount.

Sanity filters: keep a cushion, stress-test payment, compare total costs, and add “exit math” if you might move in 1–3 years.

Bottom line: Choose the tool that strengthens your balance sheet—not just your weekend plans.

Question: If you used home equity this year, which matters most?

A) One fixed, predictable payment

B) Flexible access in phases

C) Keeping my low first-mortgage rate

D) I’m not sure—need a side-by-side

Answer: Match the tool to the job.

- Cash-out refi: predictability in one loan.

- HELOC: draw only what you need, when you need it.

- Home equity loan: fixed second payment for a defined amount.

Keep a cushion, stress-test payments, and run exit math if a move is possible.

Earnest Money in Real Estate: What It Is, Why It Matters, and How to Protect It

That earnest money check shows you’re serious — but it’s also at risk. Find out how it works, when you can get it back, and what mistakes could cost you thousands.

Real Estate Due Diligence Explained: What It Is, How Much It Costs, and What Happens Next

Due diligence is more than a deposit — it’s your window to investigate the property before fully committing. Learn what it covers, how much it typically costs, and what to expect when the clock runs out.

Copied to clipboard

Manual Copy (Android email apps)

If your email app strips images when pasting: Long-press inside the box → Select all → Copy, then paste.

Rates remain volatile, inventory is shifting, and buyer options are changing in many markets. Get the quick take on what this Labor Day snapshot could mean for your next move.

By: Scott Gentry | August 15, 2025

Labor Day 2025 Housing Update: Mortgage Rates & Inventory — Is It Time to Buy?

Rates remain volatile, inventory is shifting, and buyer options are changing in many markets. Get the quick take on what this Labor Day snapshot could mean for your next move.

ProTip: Paste the post first, then remove the link and place it into the first comment. Pin it there for maximum visibility.

Option 1: Quick Win Post

Option 2: Long Form | Thought Leadership

Option 3: Interactive Question + Answer

Mortgage rates are back in the mid-6 percent range, and listings are up. Over Labor Day, buyers have leverage: more homes, fewer bidding wars, and motivated sellers.

If the payment fits your budget, now could be the time to make a move.

Rates have drifted into the mid-6 percent range, while active listings are higher than a year ago. That combo gives buyers leverage: more choice, fewer bidding wars, and negotiating power.

How to play it:

- First-time buyers: Lock if the payment fits, and ask for a float-down option before closing. Bring a fully underwritten pre-approval.

- Move-up buyers: Weigh the cost of staying (low rate, limited space) vs. moving (new payment, taxes, insurance). Target longer-days-on-market listings and ask for seller credits to buy down the rate.

- Equity-rich or cash-heavy: Push on price and concessions now; if rates dip later, refinance to optimize.

Bottom line: If the right home fits your budget, acting this Labor Day starts your equity clock sooner. You can refinance later if rates improve.

Question: If you were house-hunting this Labor Day, what matters most to you?

A) Lower mortgage rates

B) More homes to choose from

C) Negotiating power with sellers

D) Waiting to see what the Fed does next

Answer: Focus on the path that best matches your budget and timeline. If payment comfort is key, test your numbers at plus/minus 0.25 percent and ask for seller credits to buy down the rate. If selection matters, use today’s higher inventory to negotiate. Keep pre-approval current and be ready to move when quotes dip.

Video Scripts

Mortgage rates are in the mid‑6% range and inventory is up. Labor Day brings buying opportunity:

1. First‑time buyers: Know your comfort zone at +/- 0.25%. Lock now—or ask about float‑down options.

2. Move‑up buyers: Higher inventory = leverage. Negotiate hard, and ask for seller credits.

3. Equity or cash-heavy buyers: Use this market to push on price. Refinance later if rates improve.

Full breakdown is in the first comment—tap to view.

Here’s why Labor Day could be your best time to buy:

- Mid‑6% mortgage rates and a surge in inventory mean better options and negotiation power.

- First-time buyers: set your comfort range at today's quote +/‑ 0.25%, consider locking that rate or adding float‑down protection.

- Move-up buyers: with inventory up, ask for concessions on longer‑listed homes.

- Equity or all‑cash buyers: leverage this quieter market to score deals now and refinance later.

Want custom numbers based on your budget? I’ll pin a detailed comment to help you plan smart.

Tip: Post your video first, then paste your AgentID article link in the first comment and pin it.

Your Article Link:

`;

w.document.open();

w.document.write(html);

w.document.close();

}

});

})();

function copyAgentLink() {

const el = document.getElementById('s4a-agent-link');

el.select();

el.setSelectionRange(0, 999999);

navigator.clipboard.writeText(el.value).then(() => {

alert('Link copied to clipboard!');

});

}

Keeping tabs on your home’s value can guide smarter decisions. Whether you're thinking of refinancing, selling, or simply staying informed—find out when and why tracking your property’s worth matters most.

By: Scott Gentry | August 14, 2025

How Often Should You Check Your Home’s Value?

Keeping tabs on your home’s value can guide smarter decisions. Whether you're thinking of refinancing, selling, or simply staying informed—find out when and why tracking your property’s worth matters most.

Home equity can be a powerful tool—but only when used smartly. Whether you're refinancing, making home upgrades, or managing debt, discover strategies to unlock its potential in today’s market.

By: Scott Gentry | August 14, 2025

How to Use Home Equity Wisely in Today’s Market

Home equity can be a powerful tool—but only when used smartly. Whether you're refinancing, making home upgrades, or managing debt, discover strategies to unlock its potential in today’s market.

ProTip: Paste the post first, then remove the link and place it into the first comment. Pin it there for maximum visibility.

Option 1: Quick Win Post

Option 2: Long Form | Thought Leadership

Option 3: Interactive Question + Answer

Your home is more than an address—it’s also a balance sheet.

Used wisely, equity can upgrade your life; used casually, it can tighten your budget.

This guide breaks down cash-out refi, HELOC, and home equity loan—when each fits, tradeoffs, and a 10-minute decision check.

Home equity can be a powerful tool—if you match the product to the purpose.

Context: Equity grows when values rise, principal falls, or improvements add value. Before tapping it, audit your position (rate, term, timeline, cash-flow tolerance, purpose).

Smart fits:

- Cash-out refi: one fixed payment; best when your current rate isn’t far below today’s and you want predictability.

- HELOC: flexible, phase-friendly access; variable rate requires discipline.

- Home equity loan: fixed, second payment; ideal for a clear, one-time amount.

Sanity filters: keep a cushion, stress-test payment, compare total costs, and add “exit math” if you might move in 1–3 years.

Bottom line: Choose the tool that strengthens your balance sheet—not just your weekend plans.

Question: If you used home equity this year, which matters most?

A) One fixed, predictable payment

B) Flexible access in phases

C) Keeping my low first-mortgage rate

D) I’m not sure—need a side-by-side

Answer: Match the tool to the job.

- Cash-out refi: predictability in one loan.

- HELOC: draw only what you need, when you need it.

- Home equity loan: fixed second payment for a defined amount.

Keep a cushion, stress-test payments, and run exit math if a move is possible.

Video Scripts

Your home is a place and a balance sheet.

Equity is value minus what you still owe.

It grows with rising prices, principal paydown, and real improvements.

Use it thoughtfully to strengthen your finances.

Before you borrow, take inventory: value, rate, term, timeline, cash flow.

Match the tool to the job: cash-out, HELOC, or home equity loan.

Stress-test the payment and keep a cushion.

If your first-mortgage rate is low, consider a HELOC or home equity loan first.

Only green-light when the numbers fit easily.

Full guide is in the link in comments.

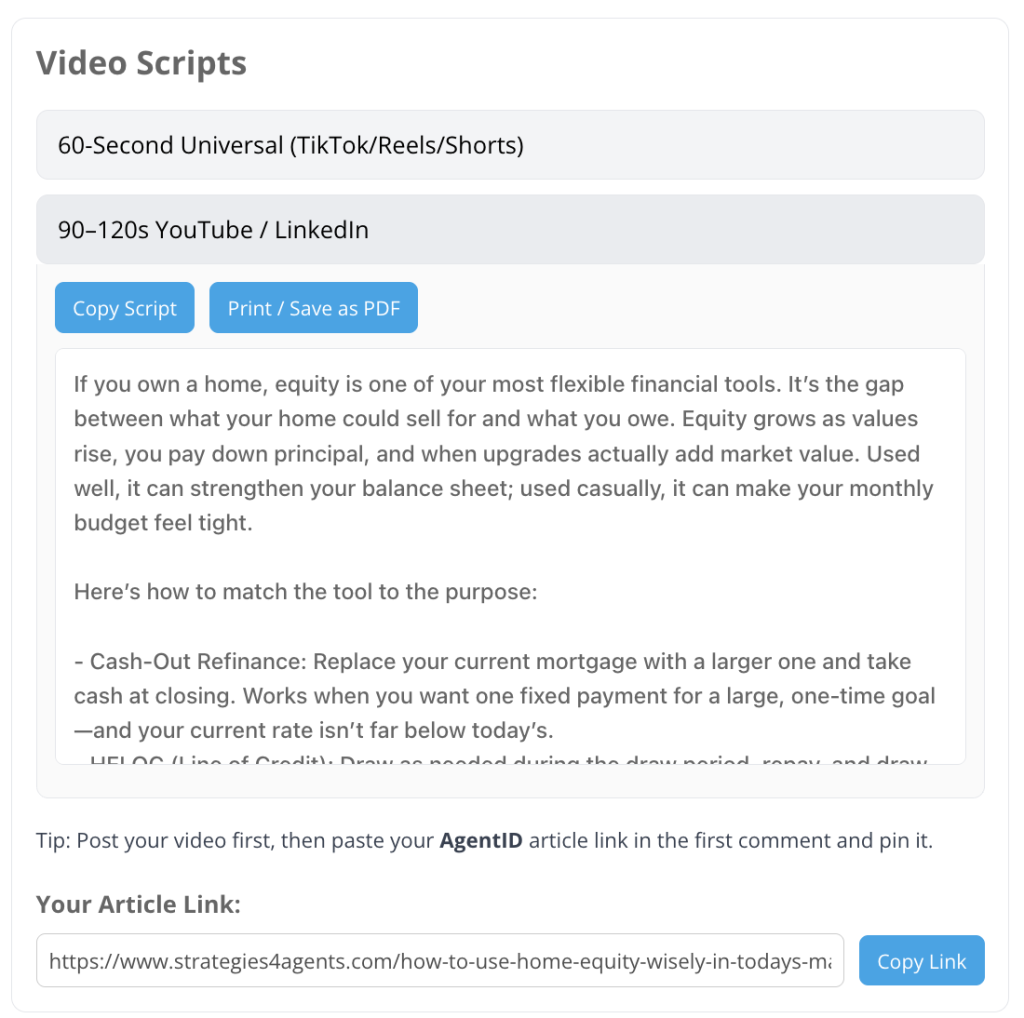

If you own a home, equity is one of your most flexible financial tools. It’s the gap between what your home could sell for and what you owe. Equity grows as values rise, you pay down principal, and when upgrades actually add market value. Used well, it can strengthen your balance sheet; used casually, it can make your monthly budget feel tight.

Here’s how to match the tool to the purpose:

- Cash-Out Refinance: Replace your current mortgage with a larger one and take cash at closing. Works when you want one fixed payment for a large, one-time goal—and your current rate isn’t far below today’s.

- HELOC (Line of Credit): Draw as needed during the draw period, repay, and draw again. Best for phased projects or an emergency back-up. Variable rates require discipline and a payment buffer.

- Home Equity Loan: A fixed-rate second loan for a clear amount. Predictable payment without touching your first mortgage—great when you know the price tag.

Before you borrow, run five “smart-use” filters:

• Keep an equity cushion beyond lender minimums.

• Confirm payment comfort—no budget squeak.

• Check time horizon—short horizons rarely justify big upfront costs.

• Validate return on use—value-adding upgrades or real interest savings.

• Respect rate reality—preserve a very low first-mortgage rate when possible.

Quick decision guide: Need flexibility in stages? Start with a HELOC. Know the exact amount and want fixed payments? Home Equity Loan. Prefer one mortgage and fixed terms—and your current rate isn’t far lower? Evaluate a Cash-Out Refi. Sitting on a very low first-mortgage rate? Compare HELOC/Home Equity Loan first.

CTA: I’ll pin the full article and a side-by-side comparison in the first comment. Comment “EQUITY” if you want a CMA and a custom plan.

Tip: Post your video first, then paste your AgentID article link in the first comment and pin it.

Your Article Link:

`;

w.document.open(); w.document.write(html); w.document.close();

}

});

// ---- Copy Link button ----

const copyLinkBtn = document.getElementById('s4a-copy-link');

if(copyLinkBtn){

copyLinkBtn.addEventListener('click', async ()=>{

try{

await navigator.clipboard.writeText(linkInput.value||'');

const prev = copyLinkBtn.textContent;

copyLinkBtn.textContent = 'Copied!';

setTimeout(()=>copyLinkBtn.textContent = prev, 1200);

}catch{

alert('Copy failed — you can copy the link manually.');

}

});

}

})();

You’ve celebrated your first year as a homeowner — now it’s time to level up. From building equity to tackling value-boosting projects, here’s how to make year two even better than the first.

By: Scott Gentry | August 14, 2025

Happy 1-Year Homeownership: Here's How to Make the Most of Year Two

You’ve celebrated your first year as a homeowner — now it’s time to level up. From building equity to tackling value-boosting projects, here’s how to make year two even better than the first.

Whether it’s been one year or many, your home deserves a little TLC. From checking smoke alarms to cleaning behind the fridge, here’s your quick checklist to keep things safe, efficient, and running smoothly.

By: Scott Gentry | August 14, 2025

Happy Home Anniversary: A Quick Check-Up for Your Home

Whether it’s been one year or many, your home deserves a little TLC. From checking smoke alarms to cleaning behind the fridge, here’s your quick checklist to keep things safe, efficient, and running smoothly.

Thinking about using your home’s equity for upgrades, debt payoff, or big goals? Learn when tapping into that value makes sense — and what to weigh before you borrow against your home.

By: Scott Gentry | July 14, 2025

Is Now the Right Time to Tap Into Your Home Equity? Here’s How to Decide

Thinking about using your home’s equity for upgrades, debt payoff, or big goals? Learn when tapping into that value makes sense — and what to weigh before you borrow against your home.

Keeping tabs on your home’s value helps with insurance, equity planning, and long-term goals. Learn how often to check, what signals matter (and which don’t), and the best tools to use.

By: Scott Gentry | August 15, 2025

Home and Market Minute

How Often Should You Check Your Home’s Value?

Keeping tabs on your home’s value helps with insurance, equity planning, and long-term goals. Learn how often to check, what signals matter (and which don’t), and the best tools to use.

Thinking HELOC, home equity loan, or cash-out refi? Compare options, costs, and smart use cases so you can put your equity to work without overextending.

Labor Day 2025 Housing Update: Mortgage Rates, Inventory & Is It Time to Buy?

Rates remain volatile, inventory is shifting, and buyer options are changing in many markets. Get the quick take on what this Labor Day snapshot could mean for your next move.

Taking the first steps toward homeownership? This guide breaks down the essential next moves, from financial preparation to working with the right professionals, so you can start your journey with confidence.

By: Scott Gentry | May 16, 2025

Homebuying Tips to Help You Succeed – Week One

You've Decided to Buy a Home—Here's What to Do Next

Taking the first steps toward homeownership? This guide breaks down the essential next moves, from financial preparation to working with the right professionals, so you can start your journey with confidence.

How to Choose the Right Neighborhood: The Ultimate Guide

Your dream home is only part of the picture—finding the right neighborhood is just as important. This guide walks you through what to consider, from schools to traffic to community vibe.

Discover why pre-approval is a must-have for homebuyers. Learn how it gives you an edge, helps you budget, and makes the process smoother from the start.

Creating a realistic homebuying budget is a critical first step toward owning your dream home. This guide walks you through hidden costs, savings, and smart strategies to stay on track.

Buying a home can be overwhelming, but it doesn’t have to be. This article provides 20 actionable tips—from budgeting and inspections to choosing the right neighborhood—to make the process smoother and stress-free.

By: Scott Gentry | May 16, 2025

Homebuying Tips to Help You Succeed – Week Two

Unlock Your Dream Home: 20 Insider Tips from Real Estate Agents

Buying a home can be overwhelming, but it doesn’t have to be. This article provides 20 actionable tips—from budgeting and inspections to choosing the right neighborhood—to make the process smoother and stress-free.

What to Look for During a Home Tour: How to Find Your Dream Home

Touring homes is exciting—but it's easy to miss important details. This guide helps you know what to look for during every walkthrough so you can spot red flags, ask the right questions, and stay focused on what matters most.

What to Ask During a Home Walkthrough: The Ultimate Buyer’s Guide

A home walkthrough is your chance to look beyond the surface and ask the right questions. This guide equips you with the essential questions to ask and details to check, helping you make an informed decision on your dream home.

Down Payment Myths for New Buyers: What You Really Need to Know

Think you need 20% down to buy a home? Think again! Learn the truth about down payment myths, alternative financing options, and how to get into your dream home faster.

Making an Offer: How to Stand Out in a Competitive Market

In a competitive real estate market, making the right offer is crucial. Learn strategies to get your offer noticed, win bidding wars, and secure your dream home.

The Ultimate Guide to Home Inspections: Types, Expectations, Timelines, and Costs

A home inspection is a crucial step in the buying process, helping buyers understand the condition of a property before closing. This guide covers different inspection types, what to expect, how long they take, and potential costs involved.

Home Appraisals Demystified: What You Need to Know

Understanding the home appraisal process is crucial for buyers and sellers alike. This guide explains the basics of appraisals, how they influence real estate transactions, and tips for preparing for a smooth appraisal process.

5 Things Mortgage Brokers Wish You Knew About Getting a Mortgage

Want to avoid delays, surprises, and stress during your mortgage process? These insider tips from loan officers shed light on what really matters—and what most homebuyers overlook.

5 Key Factors That Determine Your Mortgage Rate - What You Need to Know

Curious about what shapes your mortgage rate? Learn how your credit score, loan type, down payment, and other factors influence your interest rate. This guide simplifies complex concepts to help you make smarter financial choices and save money.

Finding the perfect mortgage doesn't have to be overwhelming. This guide simplifies the process, breaking down the key loan types, factors to consider, and strategies for making the best decision for your financial future.

By: Scott Gentry | May 16, 2025

Homebuying Tips to Help You Succeed: Week Four

Choosing the Right Mortgage for Your Needs: A Comprehensive Guide

Finding the perfect mortgage doesn't have to be overwhelming. This guide simplifies the process, breaking down the key loan types, factors to consider, and strategies for making the best decision for your financial future.

What is a Rate Lock Agreement? Pros, Cons, and What You Need to Know

A rate lock can protect you from interest rate fluctuations, but is it the right choice for you? Learn the advantages, disadvantages, and key details about rate lock agreements in this guide.

Understanding mortgage insurance is crucial for buyers weighing their options. This guide provides an in-depth explanation of PMI (Private Mortgage Insurance) and FHA MIP (Mortgage Insurance Premium), including when they're required and how they impact affordability.

Final Walkthrough Checklist: What You Need to Check Before Closing

The final walkthrough is your last chance to ensure the home is in the expected condition before closing. This checklist helps buyers avoid surprises and make sure everything is as agreed upon in the contract.

Closing costs can catch homebuyers off guard. This guide breaks down what’s included, how much you should expect to pay, and strategies to reduce your out-of-pocket expenses when finalizing your home purchase.

Thinking of selling your home? Understanding the process can help you prepare, set realistic expectations, and maximize your sale price. This guide walks you through every step, from listing to closing, so you know what to expect along the way.

By: Scott Gentry | May 16, 2025

Essential Home-Selling Insights: Your Guide to a Successful Sale – Week One

What You Should Expect When Selling Your Home

Thinking of selling your home? Understanding the process can help you prepare, set realistic expectations, and maximize your sale price. This guide walks you through every step, from listing to closing, so you know what to expect along the way.

Unlocking Your Home's Potential: A 3-Month Plan to Maximize Sale Price

Discover 10 actionable steps to prepare your home for sale over three months. From curb appeal to staging, this guide helps maximize your home's value and attract buyers.

When to Reach Out to a Real Estate Agent: The Ultimate Guide for Buyers and Sellers

Discover the key moments when buyers and sellers should connect with a real estate agent to maximize their success. From market timing to negotiation strategies, this guide covers it all.

Ready to Sell Your Home? Your Roadmap to a Successful Home Sale

Selling your home can feel overwhelming, but it doesn’t have to be. This article walks you through every step of the process, from preparing your home for showings to navigating closing day. With this guide, you’ll feel confident and ready to tackle your home sale successfully.

Setting the right price is one of the most important steps in selling your home. This article walks you through key strategies to avoid overpricing, attract more buyers, and get top-dollar offers—fast.

By: Scott Gentry | May 16, 2025

Essential Home-Selling Insights: Your Guide to a Successful Sale – Week Two

How to Price Your Home to Sell Fast

Setting the right price is one of the most important steps in selling your home. This article walks you through key strategies to avoid overpricing, attract more buyers, and get top-dollar offers—fast.

5 Costly Mistakes Home Sellers Make and How to Avoid Them

Selling a home? Avoid these five common (and costly) mistakes that can hurt your sale. Learn expert tips to sell faster, attract buyers, and maximize your home's value.

The Importance of Curb Appeal When Selling Your Home

First impressions matter—especially in real estate. This quick guide explains why curb appeal is critical and offers tips to make your home stand out before buyers even walk through the door.

How to Prepare Your Home for Sale: A Room-by-Room Checklist for Maximum Appeal

Preparing your home for sale is essential to attract buyers and get the best price. This room-by-room checklist provides practical tips to showcase your home's best features and make a lasting impression on potential buyers.

It’s almost a ground-up overhaul. First there’s a new dashboard where you can make quick posts, look for campaigns, focus on this month’s nurture ideas, or create a social media planner.

New Dashboard = Less Clicks, More Results

We’ve streamlined everything so you can jump right into action. From a single screen, instantly build your Social Planner, find content, and access your newest campaigns.

Monthly Nurture Campaigns

Nurture buyers and sellers automatically with plug-and-play monthly campaigns. Just copy and send via email, SMS, or social — done.

Quick Access to Everything

No more digging around — articles, videos, post scripts, and share buttons are right where you need them.

What Comes with Every Post (Starting Now)

Short Social Post Perfect for quick Facebook or LinkedIn updates.

Long-Form Thought Leadership Post Establish your expertise and spark engagement.

Interactive Post Option Polls, quizzes, or questions — choose your favorite, or rotate between them.

Video Scripts for YouTube and Reels Want to grow your social presence? Every post now includes scripts for vertical videos or YouTube updates — in your voice, for your audience.

Pro Tip: Pick one article a week and use all four formats to get the most mileage out of every piece of content.

These updates are live now. Head to your dashboard to check them out.

Your Branded Ad: Get Leads with Your Name, Photo & Contact Info

Every article you share could include your custom ad — showcasing your headshot, logo, and contact details to build trust and capture leads effortlessly.

About six months out? This quick checklist covers credit tune-ups, budgeting with realistic payments, building cash for down payment and closing costs, and getting lender-ready—so you can move fast when the right home appears.

ProTip: Paste the post first, then remove the link and place it into the first comment. Pin it there for maximum visibility.

Option 1: Quick Win Post

Buying a home in ~6 months? Here’s your quick plan:

• Month 1: Pull all 3 credit reports, dispute errors, set a realistic budget.

• Month 2: Automate savings to a dedicated account; trim non-essentials.

• Month 3: Research neighborhoods, track prices, tour a few open houses.

• Month 4: Get pre-approved; gather tax returns, pay stubs, bank/asset statements.

• Month 5: Avoid big purchases or new credit; reinforce your emergency fund.

• Month 6: Choose your agent, line up an inspector/attorney (if needed), and prep to write offers.

Full guide in the link.

Option 2: Long Form | Thought Leadership

Six months out is the sweet spot to de-risk homebuying:

• Financial readiness: Review all three credit reports, calculate DTI, and budget for down payment, closing costs, and moving.

• Savings engine: Automate transfers, trim recurring spend, consider a side gig for extra cushion.

• Market research: Compare neighborhoods by commute, schools, amenities; monitor list-to-sale dynamics and price trends.

• Lender power: Shop lenders, organize docs (W-2s, pay stubs, bank/asset statements), and secure a pre-approval.

• Risk control: Pause big purchases, avoid opening new credit, keep employment steady, and build a 3–6 month buffer.

• Team up: Hire a local agent; consider a real estate attorney (state-dependent) and line up a thorough inspector.

Preparation now = smoother offers, cleaner underwriting, and fewer surprises at closing.

Option 3: Interactive Q&A

Question: If you’re ~6 months from buying, what’s your top priority today?

A) Clean up credit & set a budget

B) Automate savings for down & closing

C) Research neighborhoods & price trends

D) Get a real pre-approval and organize docs

Answer: Pick the lever that shortens your path. Clear credit issues, build cash automatically, study the market, and lock a legit pre-approval so you can act fast when the right home hits.

Video Scripts

Tip: Post your video first, then paste your AgentID article link in the first comment and pin it.

Buying a home in about 6 months? Here’s your fast-track plan:

Month 1: Pull all 3 credit reports, fix errors, calculate your DTI, and set a realistic savings/budget target.

Month 2: Automate transfers into a dedicated home fund; trim subscriptions and non-essentials.

Month 3: Research neighborhoods—commute, schools, amenities—and track price trends. Tour a few open houses.

Month 4: Get pre-approved. Gather W-2s, pay stubs, tax returns, bank/asset statements, and debt details.

Month 5: Avoid big purchases or new credit, keep job stability, and pad a 3–6 month emergency fund.

Month 6: Choose your agent, line up an inspector (and attorney if required), and get offer-ready.

Full 6-month guide is pinned in the first comment—tap to view.

If your goal is to buy in roughly six months, here’s the step-by-step that de-risks the process:

• Month 1 — Assess Readiness: Pull Equifax, Experian, and TransUnion; dispute inaccuracies. Calculate DTI and set a monthly savings target for down payment, closing costs, and moving.

• Month 2 — Build Savings: Automate transfers into a dedicated account. Trim recurring spend and consider a small side gig to boost your cushion.

• Month 3 — Study the Market: Compare neighborhoods for commute, schools, amenities, safety, and future development. Track list vs. sale dynamics and price trends; visit open houses to refine your must-haves.

• Month 4 — Pre-Approval: Shop lenders and gather documents—W-2s, pay stubs, two years of tax returns, bank/asset statements, and debt info. A strong pre-approval focuses your search and strengthens offers.

• Month 5 — Minimize Risk: Avoid large purchases and new credit lines; maintain job stability; build a 3–6 month emergency fund to handle surprises during underwriting.

• Month 6 — Assemble the Team: Hire a local agent, line up a thorough home inspector, and consider an attorney where required. You’re now ready to write clean, competitive offers.

I’ll pin the full article and checklist in the first comment—use it to move from planning to keys with fewer surprises.

You’ve Decided to Buy a Home: Here’s What to Do Next

placeholder dummy

Ready to start house hunting? Before open houses, build a strong foundation: tighten credit and savings, get pre-approved, define must-haves vs. deal-breakers, organize documents, and avoid common pitfalls like opening new credit or changing jobs. This guide walks you through each step so you can shop confidently and close smoothly.

ProTip: Paste the post first, then remove the link and place it into the first comment. Pin it there for maximum visibility.

Option 1: Quick Win Post

You’ve decided to buy a home—now what?

• Step 1: Credit & cash — review all three reports, fix errors, aim higher on score, pause big purchases.

• Step 2: Pre-approval — gather pay stubs, W-2s, bank statements, and shop lenders.

• Step 3: Define needs — must-haves, nice-to-haves, deal-breakers; research neighborhoods.

• Step 4: Get organized — keep docs in one digital folder; add proof of any extra income.

• Step 5: Avoid pitfalls — don’t change jobs or open new credit; stick to your budget.

• Step 6: Choose the right agent — and plan for surprises (appraisal, inspection, timelines).

Full guide below.

Option 2: Long Form | Thought Leadership

Buying a home starts long before the first open house. Here’s the foundation that makes the rest easy:

• Financial health: Check your credit report for errors, target the best pricing, and hold off on big purchases that can inflate your DTI.

• Pre-approval as your “ticket”: Provide pay stubs, W-2s, tax returns, bank/asset statements, and debt details. A strong letter focuses your search and strengthens offers.

• Define the target: Clarify must-haves vs. nice-to-haves and deal-breakers. Research commute, schools, amenities, and future development.

• Paperwork ready: Centralize documents (and proof of extra income) to reduce underwriting friction.

• Avoid common mistakes: Don’t switch jobs, don’t open new credit lines, and don’t stretch beyond your comfort payment.

• Think ahead: Layout for remote work or a growing family, location for potential appreciation, and features that help resale.

Preparation now = smoother escrow later.

Option 3: Interactive Q&A

Question: After deciding to buy, what’s your first move?

A) Clean up credit & build reserves

B) Get a full pre-approval

C) Define must-haves & target neighborhoods

D) Gather pay stubs, W-2s, and bank statements

Answer: Pick the step that removes your biggest bottleneck. Clean credit + real pre-approval + organized docs = stronger offers when the right home appears.

Video Scripts

Tip: Post your video first, then paste your AgentID article link in the first comment and pin it.

You’ve decided to buy a home—now what? Here’s the fast-start plan:

1) Get your financial house in order: check all three credit reports, aim higher on score, pay down balances, and pause big purchases.

2) Get pre-approved: gather pay stubs, W-2s, 2 years of tax returns, bank/asset statements, and debt details. Shop homes after the letter is in hand.

3) Define your target: must-haves vs. nice-to-haves vs. deal-breakers. Research neighborhoods for commute, schools, amenities, and safety.

4) Organize documents: one digital folder for everything, including proof of bonuses or other income.

5) Avoid pitfalls: don’t change jobs, don’t open new credit, and don’t stretch beyond your comfort payment.

6) Think long-term: layout for remote work or a growing family, resale potential, and choose a great agent.

I’ll pin the full guide in the first comment—use it to shop smart and close smoothly.

You’ve decided it’s time to buy a home. Before the open houses, build your foundation:

• Step 1 — Financial Health: Pull all three credit reports, dispute errors, and aim higher on score for better pricing. Pause big-ticket purchases so your DTI stays clean and your approval isn’t jeopardized. Build savings for down payment, closing costs, and an emergency fund.

• Step 2 — Pre-Approval: Treat it like your golden ticket. Collect pay stubs, W-2s, 2 years of tax returns, bank/asset statements, and debt details. Lenders may verify employment. A strong letter keeps you focused on the right price range and strengthens offers.

• Step 3 — Define the Target: Make a clear list—must-haves, nice-to-haves, and deal-breakers. Research neighborhoods for commute, schools, amenities, safety, and future development. Think about how you’ll live there, not just the list price.

• Step 4 — Paperwork Ready: Centralize documents in one digital folder, including proof of bonuses, alimony, or other income sources. Staying organized prevents underwriting delays.

• Step 5 — Avoid Pitfalls: Don’t change jobs mid-process, don’t open new credit lines, and don’t spend to the max just because you’re approved. Stick to a realistic, all-in monthly budget.

• Step 6 — Future Potential: Look beyond today—layout for remote work or a growing family, features that support resale, and areas with sound appreciation potential.

• Step 7 — The Right Agent: An experienced agent helps you navigate inventory, negotiate effectively, and manage inspections, contracts, and closing timelines.

• Step 8 — Plan for the Unexpected: Be ready for bidding wars, appraisal gaps, or timing hiccups. Have a contingency plan so surprises don’t derail your goals.

I’ll pin the full article in the first comment—use it as your step-by-step guide from decision to keys.

What You Need to Do Today If You’re Buying a Home in 12 Months

placeholder dummy

Ready to buy in a year? This month-by-month game plan covers credit, saving for down payment and closing costs, getting pre-approved, and touring smart—so you’re confident when it’s time to make an offer.

ProTip: Paste the post first, then remove the link and place it into the first comment. Pin it there for maximum visibility.

Option 1: Quick Win Post

Buying in the next 12 months? Start now.

• Month 1: Pull your credit and dispute errors. Aim 700+.

• Months 2–3: Automate savings for down payment + closing costs.

• Months 4–5: Pay down high-interest debt. No new accounts.

• Months 6–7: Set a realistic budget (taxes, insurance, HOA).

• Months 8–9: Get pre-approved and gather docs.

• Months 10–11: Tour with a great agent and take notes.

• Month 12: Make an offer, inspect, close.

Your 1-year plan to get the keys.

Option 2: Long Form | Thought Leadership

A 12-month runway to homeownership beats rushing at the finish line. Here’s the framework I recommend clients follow:

• Credit first (Month 1): Pull all three reports, fix errors, target 700+ for better pricing.

• Liquidity (Months 2–3): Automate savings for down payment and 2–5% closing costs. Trim subscriptions and redirect windfalls.

• De-risk (Months 4–5): Pay down high-interest debt to improve DTI; avoid opening new credit.

• Reality check (Months 6–7): Model payment scenarios including taxes, insurance, HOA, and maintenance. Pressure-test at ±0.25% rate.

• Lender readiness (Months 8–9): Shop lenders, secure pre-approval, and keep docs in a shared folder.

• Execution (Months 10–11): Tour strategically, focus on days-on-market and price history, document pros/cons.

• Close strong (Month 12): Write a competitive offer inside your budget, order inspection, negotiate credits, and close.

Start the equity clock sooner—plan, then act.

Option 3: Interactive Q&A

Question: If you want to buy a home in 12 months, what’s your biggest focus today?

A) Getting my credit to 700+

B) Building a bigger down payment

C) Locking in a realistic monthly budget

D) Getting pre-approved and gathering docs

Answer: Pick the lever that moves your timeline most. Clean up credit errors, automate savings, price your monthly payment with taxes/insurance, and get pre-approved so you can act quickly when the right home appears.

Video Scripts

Tip: Post your video first, then paste your AgentID article link in the first comment and pin it.

Buying a home in the next 12 months? Here’s your month-by-month game plan:

Month 1: Pull your credit from all three bureaus, fix errors, and target 700+.

Months 2–3: Automate savings for down payment + 2–5% closing costs.

Months 4–5: Pay down high-interest debt; avoid opening new accounts.

Months 6–7: Build a realistic budget with taxes, insurance, HOA, and maintenance.

Months 8–9: Shop lenders, get pre-approved, and organize docs in one folder.

Months 10–11: Tour with a great agent, track days-on-market, and take notes.

Month 12: Make a competitive offer, schedule inspection, negotiate credits, close.

Full 12-month checklist is pinned in the first comment—tap to view.

If you want keys in your hand 12 months from now, start with a simple runway:

• Month 1 — Credit First: Pull all three reports, dispute errors, and aim for a 700+ score for better pricing.

• Months 2–3 — Liquidity: Automate transfers into savings for down payment and 2–5% closing costs. Trim subscriptions and redirect windfalls.

• Months 4–5 — De-Risk: Pay down high-interest balances to improve your DTI. Avoid new credit lines.

• Months 6–7 — Reality Check: Price your monthly payment with taxes/insurance/HOA/maintenance. Stress-test at ±0.25% on rates.

• Months 8–9 — Lender Ready: Shop lenders, lock a pre-approval, keep pay stubs, W-2s, and statements in a shared folder.

• Months 10–11 — Execution: Tour intentionally. Watch days-on-market and price history. Track pros/cons to compare clearly.

• Month 12 — Close Strong: Write a competitive offer within budget, order inspection, negotiate credits to buy down your rate, and close.

I’ll pin the full article and checklist in the first comment—use it to stay on track all year.

Labor Day 2025 Housing Update: Mortgage Rates & Inventory — Is It Time to Buy?

placeholder dummy

Rates remain volatile, inventory is shifting, and buyer options are changing in many markets. Get the quick take on what this Labor Day snapshot could mean for your next move.

ProTip: Paste the post first, then remove the link and place it into the first comment. Pin it there for maximum visibility.

Option 1: Quick Win Post

Mortgage rates are back in the mid-6 percent range, and listings are up. Over Labor Day, buyers have leverage: more homes, fewer bidding wars, and motivated sellers.

If the payment fits your budget, now could be the time to make a move.

Option 2: Long Form | Thought Leadership

Rates have drifted into the mid-6 percent range, while active listings are higher than a year ago. That combo gives buyers leverage: more choice, fewer bidding wars, and negotiating power.

How to play it:

- First-time buyers: Lock if the payment fits, and ask for a float-down option before closing. Bring a fully underwritten pre-approval.

- Move-up buyers: Weigh the cost of staying (low rate, limited space) vs. moving (new payment, taxes, insurance). Target longer-days-on-market listings and ask for seller credits to buy down the rate.

- Equity-rich or cash-heavy: Push on price and concessions now; if rates dip later, refinance to optimize.

Bottom line: If the right home fits your budget, acting this Labor Day starts your equity clock sooner. You can refinance later if rates improve.

Option 3: Interactive Q&A

Question: If you were house-hunting this Labor Day, what matters most to you?

A) Lower mortgage rates

B) More homes to choose from

C) Negotiating power with sellers

D) Waiting to see what the Fed does next

Answer: Focus on the path that best matches your budget and timeline. If payment comfort is key, test your numbers at plus/minus 0.25 percent and ask for seller credits to buy down the rate. If selection matters, use today’s higher inventory to negotiate. Keep pre-approval current and be ready to move when quotes dip.

Video Scripts

Tip: Post your video first, then paste your AgentID article link in the first comment and pin it.

Mortgage rates are in the mid‑6% range and inventory is up. Labor Day brings buying opportunity:

1. First‑time buyers: Know your comfort zone at +/- 0.25%. Lock now—or ask about float‑down options.

2. Move‑up buyers: Higher inventory = leverage. Negotiate hard, and ask for seller credits.

3. Equity or cash-heavy buyers: Use this market to push on price. Refinance later if rates improve.

Full breakdown is in the first comment—tap to view.

Here’s why Labor Day could be your best time to buy:

- Mid‑6% mortgage rates and a surge in inventory mean better options and negotiation power.

- First-time buyers: set your comfort range at today's quote +/‑ 0.25%, consider locking that rate or adding float‑down protection.

- Move-up buyers: with inventory up, ask for concessions on longer‑listed homes.

- Equity or all‑cash buyers: leverage this quieter market to score deals now and refinance later.

Want custom numbers based on your budget? I’ll pin a detailed comment to help you plan smart.

Keeping tabs on your home’s value helps with insurance, equity planning, and long-term goals. Learn how often to check, what signals matter (and which don’t), and the best tools to use.

Thinking HELOC, home equity loan, or cash-out refi? Compare options, costs, and smart use cases so you can put your equity to work without overextending.

Labor Day 2025 Housing Update: Mortgage Rates, Inventory & Is It Time to Buy?

Rates remain volatile, inventory is shifting, and buyer options are changing in many markets. Get the quick take on what this Labor Day snapshot could mean for your next move.

By: Scott Gentry |

Published: August 14, 2025 |

Categories:

Nurture Past Clients

How Often Should You Check Your Home’s Value?

placeholder dummy

Keeping tabs on your home’s value can guide smarter decisions. Whether you’re thinking of refinancing, selling, or simply staying informed—find out when and why tracking your property’s worth matters most.

Rates remain volatile, inventory is shifting, and buyer options are changing in many markets. Get the quick take on what this Labor Day snapshot could mean for your next move.

By: Scott Gentry | August 15, 2025

Labor Day 2025 Housing Update: Mortgage Rates & Inventory — Is It Time to Buy?

Rates remain volatile, inventory is shifting, and buyer options are changing in many markets. Get the quick take on what this Labor Day snapshot could mean for your next move.

ProTip: Paste the post first, then remove the link and place it into the first comment. Pin it there for maximum visibility.

Option 1: Quick Win Post

Option 2: Long Form | Thought Leadership

Option 3: Interactive Question + Answer

Mortgage rates are back in the mid-6 percent range, and listings are up. Over Labor Day, buyers have leverage: more homes, fewer bidding wars, and motivated sellers.

If the payment fits your budget, now could be the time to make a move.

Rates have drifted into the mid-6 percent range, while active listings are higher than a year ago. That combo gives buyers leverage: more choice, fewer bidding wars, and negotiating power.

How to play it:

- First-time buyers: Lock if the payment fits, and ask for a float-down option before closing. Bring a fully underwritten pre-approval.

- Move-up buyers: Weigh the cost of staying (low rate, limited space) vs. moving (new payment, taxes, insurance). Target longer-days-on-market listings and ask for seller credits to buy down the rate.

- Equity-rich or cash-heavy: Push on price and concessions now; if rates dip later, refinance to optimize.

Bottom line: If the right home fits your budget, acting this Labor Day starts your equity clock sooner. You can refinance later if rates improve.

Question: If you were house-hunting this Labor Day, what matters most to you?

A) Lower mortgage rates

B) More homes to choose from

C) Negotiating power with sellers

D) Waiting to see what the Fed does next

Answer: Focus on the path that best matches your budget and timeline. If payment comfort is key, test your numbers at plus/minus 0.25 percent and ask for seller credits to buy down the rate. If selection matters, use today’s higher inventory to negotiate. Keep pre-approval current and be ready to move when quotes dip.

Video Scripts

Mortgage rates are in the mid‑6% range and inventory is up. Labor Day brings buying opportunity:

1. First‑time buyers: Know your comfort zone at +/- 0.25%. Lock now—or ask about float‑down options.

2. Move‑up buyers: Higher inventory = leverage. Negotiate hard, and ask for seller credits.

3. Equity or cash-heavy buyers: Use this market to push on price. Refinance later if rates improve.

Full breakdown is in the first comment—tap to view.

Here’s why Labor Day could be your best time to buy:

- Mid‑6% mortgage rates and a surge in inventory mean better options and negotiation power.

- First-time buyers: set your comfort range at today's quote +/‑ 0.25%, consider locking that rate or adding float‑down protection.

- Move-up buyers: with inventory up, ask for concessions on longer‑listed homes.

- Equity or all‑cash buyers: leverage this quieter market to score deals now and refinance later.

Want custom numbers based on your budget? I’ll pin a detailed comment to help you plan smart.

Tip: Post your video first, then paste your AgentID article link in the first comment and pin it.

Your Article Link:

`;

w.document.open();

w.document.write(html);

w.document.close();

}

});

})();

function copyAgentLink() {

const el = document.getElementById('s4a-agent-link');

el.select();

el.setSelectionRange(0, 999999);

navigator.clipboard.writeText(el.value).then(() => {

alert('Link copied to clipboard!');

});

}

Keeping tabs on your home’s value helps with insurance, equity planning, and long-term goals. Learn how often to check, what signals matter (and which don’t), and the best tools to use.

By: Scott Gentry | August 15, 2025

Home and Market Minute

How Often Should You Check Your Home’s Value?

Keeping tabs on your home’s value helps with insurance, equity planning, and long-term goals. Learn how often to check, what signals matter (and which don’t), and the best tools to use.

Thinking HELOC, home equity loan, or cash-out refi? Compare options, costs, and smart use cases so you can put your equity to work without overextending.

Labor Day 2025 Housing Update: Mortgage Rates, Inventory & Is It Time to Buy?

Rates remain volatile, inventory is shifting, and buyer options are changing in many markets. Get the quick take on what this Labor Day snapshot could mean for your next move.

Thinking of buying before year-end? August is the perfect time to get serious. Learn why late summer can give you an edge — and what steps to take now to close before the holidays.

By: Scott Gentry | July 28, 2025

Is It Too Late to Buy a Home This Year? Not If You Start in August

Thinking of buying before year-end? August is the perfect time to get serious. Learn why late summer can give you an edge — and what steps to take now to close before the holidays.

Want to add instant appeal — and value — to your home this season? These budget-friendly outdoor projects can make your yard, porch, or patio shine, whether you’re staying put or thinking of selling soon.

By: Scott Gentry | July 7, 2025

Easy Outdoor Projects to Boost Your Home’s Value This Summer

Want to add instant appeal — and value — to your home this season? These budget-friendly outdoor projects can make your yard, porch, or patio shine, whether you’re staying put or thinking of selling soon.

Keep your home in top shape this summer! From gutters to HVAC and curb appeal, this easy-to-follow checklist helps you tackle seasonal tasks that protect your investment and avoid costly surprises down the road.

By: Scott Gentry | July 7, 2025

Your Essential Summer Home Maintenance Checklist

Keep your home in top shape this summer! From gutters to HVAC and curb appeal, this easy-to-follow checklist helps you tackle seasonal tasks that protect your investment and avoid costly surprises down the road.

Thinking about buying a home this summer? July can be a sweet spot for deals, less competition, and moving before school starts. Here’s why you might still have time to score the right home and the right rate.

By: Scott Gentry | July 7, 2025

Why July Is One of the Best Times to Buy a House — and Why It’s Not Too Late!

Thinking about buying a home this summer? July can be a sweet spot for deals, less competition, and moving before school starts. Here’s why you might still have time to score the right home and the right rate.

There’s a myth in real estate that success comes from working harder. But top agents know better. They’re not grinding out 80-hour weeks or constantly reinventing their marketing. They’ve simply figured out how to work smarter—with systems, shortcuts, and strategies...